Green Bond Tokens — A New Paradigm in Carbon Finance

The carbon financing chain is broken. While the general consensus among companies is in favor of reducing their carbon footprint, executing green initiatives tends to be capital intensive and often does not yield immediate returns. Bond issuance appears to be an appropriate financing mechanism on the surface, but the process is notoriously expensive. The result is that companies that choose to issue bonds are much more likely to do so for endeavors that will drive more immediate revenue. Lately, the concept of “green bonds,” or bonds with proceeds specifically earmarked for sustainability purposes, has gained traction, but it faces logistical challenges in staying transparent with where the money actually goes.

Enter green bond tokens: blockchain-based bonds designed to enable greenhouse gas reduction efforts of all sizes. They simultaneously solve for the cost problem facing would-be issuers and the transparency problem facing potential buyers. Moreover, as tokens on a distributed ledger, they carry the potential for new functionality uniquely available to digital assets over traditional ones.

What Makes a Green Bond Green?

For the purposes of this piece, a bond has three important characteristics: coupon rate, which is the amount paid per period, payment schedule, which defines the length of that period, and maturity, which is how long the holder receives payments for. For example, a 10-year bond with a $1000 par (initial) value, 5% annual coupon, and payment schedule of 6 months would pay $25, twice a year, for a 10-year duration. When you hear about a company “issuing debt” or “issuing credit”, it usually means they are selling bonds.

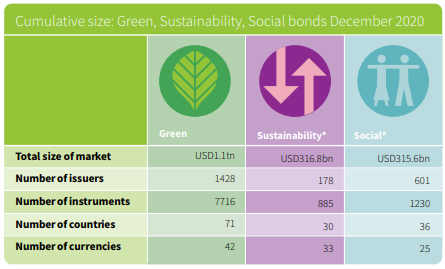

Green bonds are the same as traditional bonds, except the proceeds ostensibly go toward some environmental initiative. They are part of a larger bond category known as “Sustainability”, which also includes social (supporting societal improvements like housing or public health) and sustainability (some combination of the aforementioned green and social benefits) bonds.

Within the Sustainability category, green bonds command the largest market size at USD $1.1 trillion.

Green bonds are labeled as such when the issuer clearly indicates that the proceeds will be used solely to finance projects with positive environmental outcomes. However, a report by VanEck states that there is no market-wide database of green or green-eligible bonds, and indeed many of those that are issued have been “self-labeled.” Lacking central verification dilutes the authority of the label, which may lead to slower adoption and eventual tangible environmental consequences. In 2014, The International Capital Market Association (ICMA) created a unified standard called the “Green Bond Principles”. While the tenets are not centrally enforced, they lay a framework for a commonly understood set of criteria that defines “greenness”. They are:

Use of proceeds: Proceeds should fund projects with clear environmental benefits, with clear disclosure in legal documentation

Project evaluation and selection: Issuers should outline a process to determine project eligibility and sustainability objectives

Management of proceeds: Proceeds should be ringfenced or tracked through a formal internal process

Reporting: Annual disclosure of the use of proceeds and qualitative and quantitative performance measures

Bonds on the Blockchain

At its core, a green bond is a financial instrument governed by a set of rules such as how its proceeds can be deployed, its payment schedule, and its coupon rate. Putting a bond put onto the blockchain through the process of tokenization allows these rules to be coded in directly and enforced programmatically. Doing so makes the process cheaper and more repeatable for issuers, while purchasers receive transparency guarantees from the code that governs the bond’s behavior being open-source.

Issuer Benefits

According to an HSBC report, by delegating to code what would usually be part of an expensive legal process, bond issuance costs can be reduced by a factor of nearly 10x. These savings can manifest as higher interest rates for buyers or direct reinvestments into the green initiatives themselves for issuers:

For a more technical look at how the code may be implemented for green bonds specifically, a team of researchers from Greece published an in-depth paper on the topic in 2020. The core functions are reproduced below:

With tokenization lowering the price of bond issuance, more entities will be empowered to take part in a wider range of projects. It lowers the barrier of entry for large projects, while making smaller ones economically viable through drastically reduced fixed costs. More projects by more players, in turn, will have a tangible impact on the amount of greenhouse gas in our atmosphere.

While this would cause a spike in bond supply, the expectation is that demand would grow to match. Having the bonds as blockchain-native assets makes offering them on secondary markets frictionless and gives them exposure to the entire crypto trading sector.

Holder Benefits

Tokenization makes bonds materially more accessible for issuers, but the benefits extend to buyers as well. Payouts, for example, are made seamless.

Additionally, tokenization can allow for completely new functionalities that traditional bonds never could have, like governance. Whereas holders of traditional bonds are somewhat bystanders, unable to influence the activity of the issuing company, tokens can have governance mechanisms built in. In other words, holders can be empowered to actively keep issuers accountable for upholding ICMA Green Bond Principles.

Periodic Coupon Payments

The coupon rate paid to holders in regular intervals is the primary incentive for purchasing traditional bonds, and is ideally funded with income derived from whatever activity the issuer took on debt for in the first place.

The simplest implementation of a tokenized green bond would serve this same purpose, but more efficiently. A record of bondholders is natively maintained on the blockchain, and the value and period of payouts can be coded in. This allows ownership of a bond token to serve as proof that the bearer is entitled to its benefits, which in turn can be programmatically distributed.

Interest payments could come in the form of a stablecoin denomination, either from the net savings achieved by switching to renewable energy, or from the sale of carbon credits earned.

…the form of the payout is another place where green bond token issuers can innovate.

However, because any asset can live on a blockchain, the form of the payout is another place where green bond token issuers can innovate. One can imagine a future where carbon credits themselves are a globally leading commodity. If the project that an issuer’s green bonds were issued for produces credits, using those to make coupon payments instead would not only eliminate conversion costs, but may also make the bond more desirable as its holders would gain exposure to a popular asset class.

Similarly, in the future a company’s value will likely be (partially) tied to its carbon emissions. In this case, executing green projects has a first-order impact on the stock price. To align incentives, the company may choose to pay its bondholders in tokenized company equity instead of a national currency.

Governance

The ICMA has already done the hard work to define the requirements for a green bond, but the criteria are all not strictly quantitative. In this case, it should fall on the token holders (and therefore stakeholders) to decide if they are happy with how the tenets are being upheld. A green bond token can have mechanisms for holders to exercise governance.

One potential way to implement oversight is by preventing the issuer from accessing all the funds at once. In this model, all funds remain locked in the smart contract and are only released to the issuer in chunks over time. The issuer would publish a regular report with third-party attestations showing exactly how they are complying with ICMA guidelines. If bondholders are unhappy with the process or progress, they can cash out from the pool of remaining funds. This way, issuers are forced to not only put together a thoughtful roadmap to support initial sales, but also maintain transparency throughout the life of their project(s).

This flexibility could give rise to a “green investment corporation” that pools buyer funds and allocates them to projects that they deem most impactful, in real time.

The biggest advantage of the above approach is that it scales to any type of bond issuer. A single corporation issuing a bond to capitalize a single project is the simplest use case. But what about an entity whose business is investing in green projects? They may operate more like a venture fund, raising money first and selecting projects later. As long as they set the appropriate expectations at issuance time, people can buy in the same way they might buy into an IPO. In either case, investors are protected. This flexibility could give rise to a “green investment corporation” that pools buyer funds and allocates them to projects that they deem most impactful, in real time.

Lastly, tokenized bonds have the potential to give holders not only insight into the investment process, but also an active hand in managing it. The above scenario describes a central body delegating capital to projects based on their in-house expertise, but the bond token could also contain a function that allows buyers to earmark their funds only for a specific project or type of project. Alternatively, there could be a voting mechanism whereby holders are presented with a list of projects, and the decision for what to fund would occur democratically. This allows the “green investment corporation” to realize a more distributed form as an “autonomous green investment vehicle”.

Conclusion

Tokenized green bonds have the potential to change the financing paradigm for green projects. Not only do they make any capital more readily available to entities that wish to run initiatives of any given size, but they also open the market to a massive number of new potential participants. By governing how funds are spent, they can help enforce the transparency standards the ICMA has created while protecting investors. A tokenized bond can do everything a traditional bond can at a fraction of the price, while introducing innovations like custom coupons and autonomous green investment vehicles that make it superior.